November 17, 2025

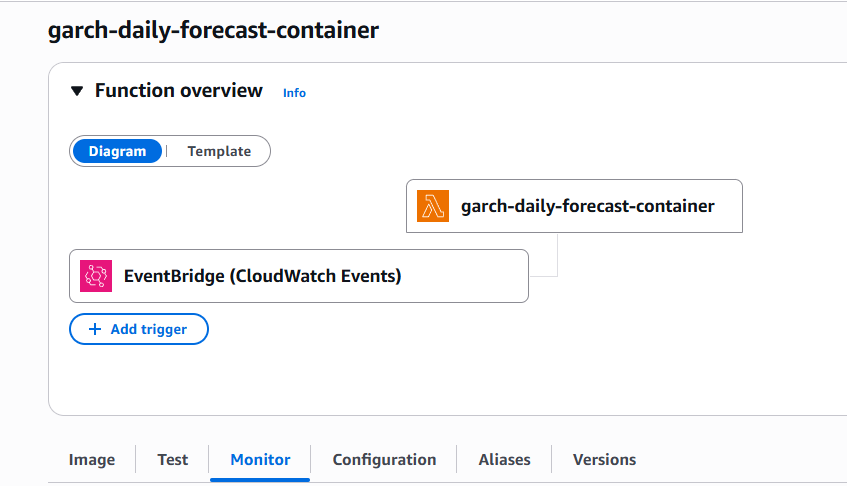

From Static Analysis to Live Dashboard: Automating GARCH Models for Real-Time Volatility Tracking with AWS

Narrative on transforming static GARCH model into live dashboard using AWS Lambda, Docker containers, and S3 automation despite dependency nightmares.

November 11, 2025

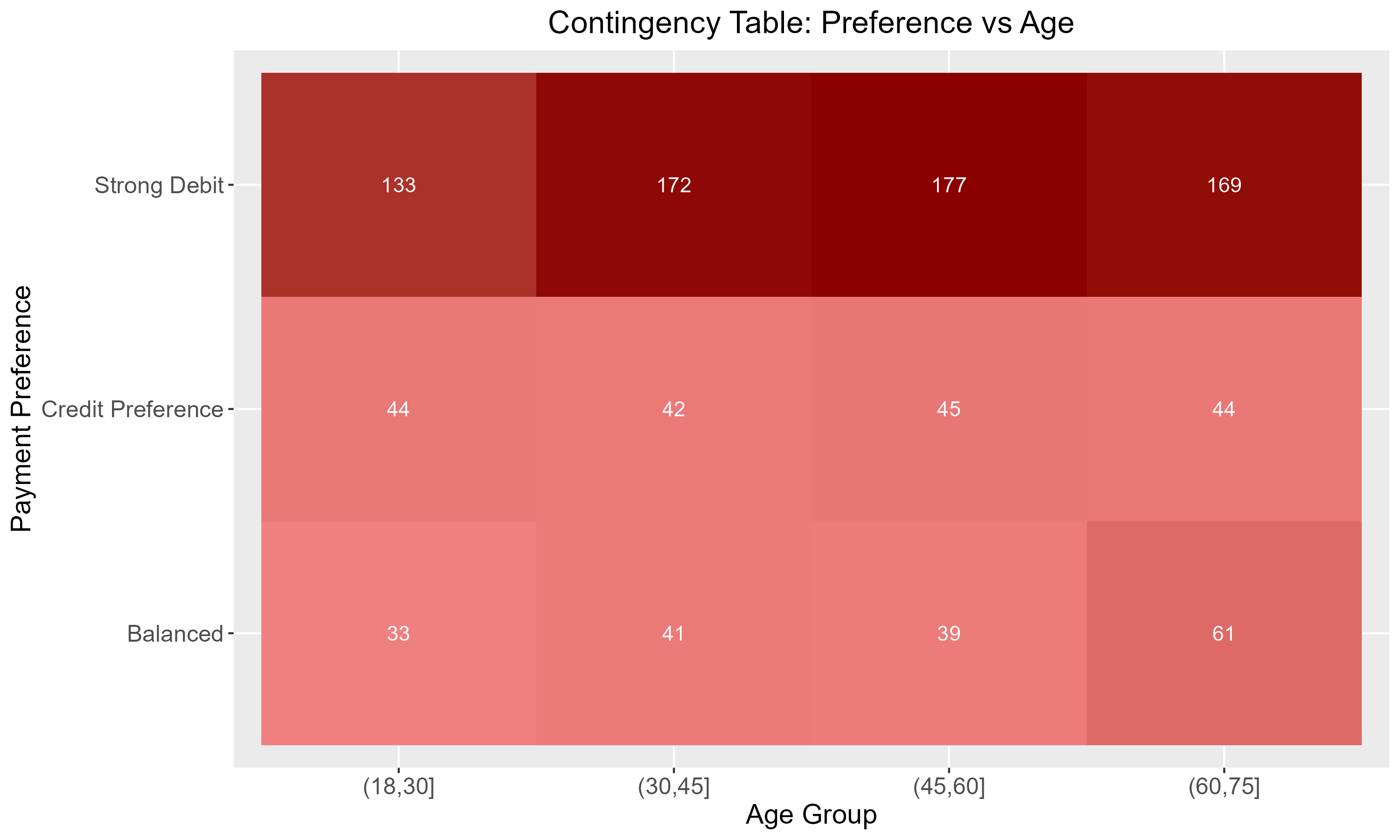

Back to Basics: Chi-Squared Test with R

Brief overview of creating a Chi-Squared to test to determine if two categorical groups are independent.

November 10, 2025

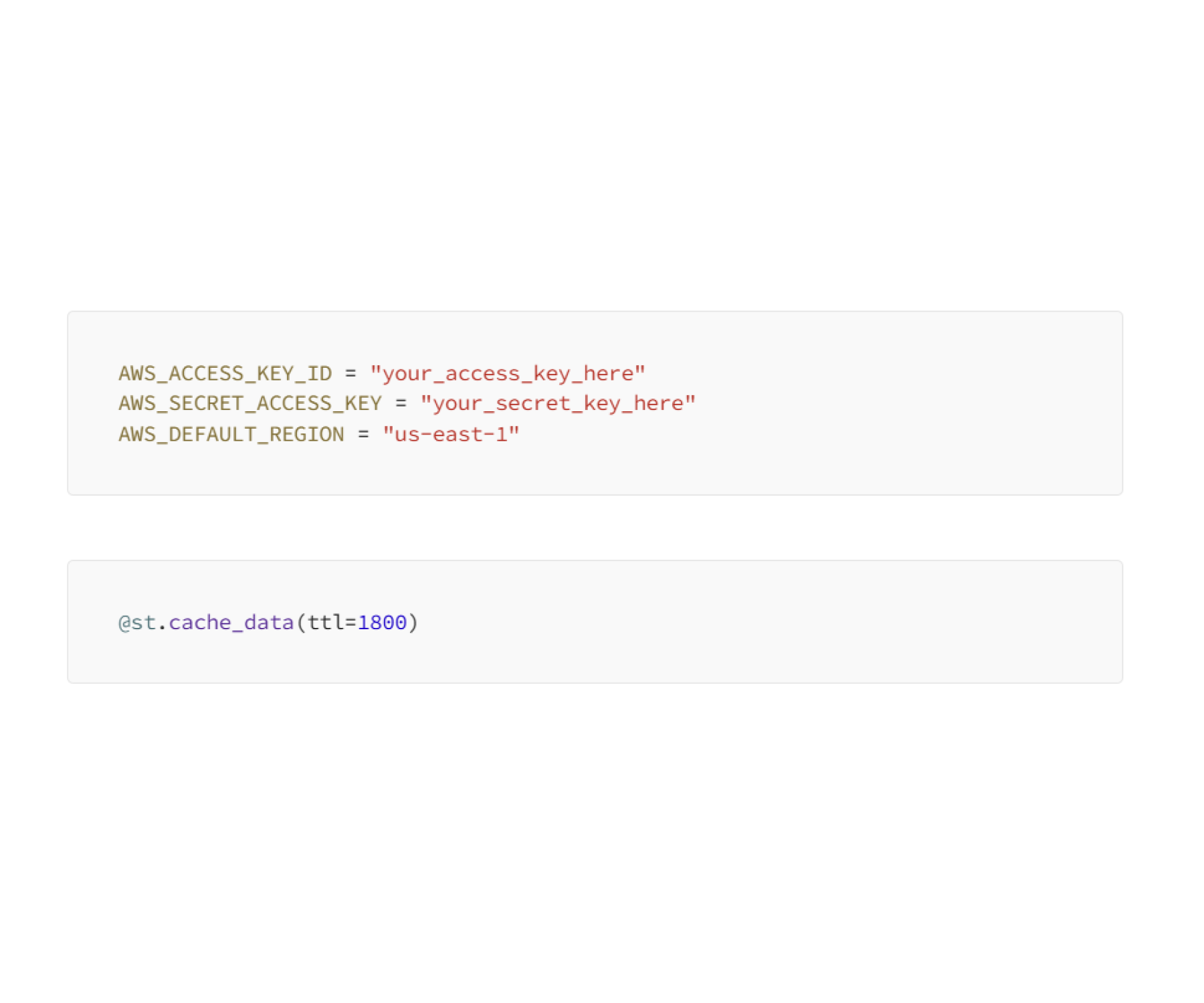

QUICK HITS: SECRETS and Cache Settings in Streamlit

Brief look at setting up SECRETS in Streamlit and setting cache "time to live" settings.

October 29, 2025

Back to Basics: CDF and PDF with R

Brief introduction to leveraging Cumulative Distribution Functions and Probability Density Functions for statistical analysis in R.

October 8, 2025

Beyond the Algorithm: How to Turn Clustering into Actionable Customer Profiles

Brief overview of analytical frameworks for turning broad problem statements into actionable business intelligence.

September 25, 2025

Back to Basics: KNN with R

KNN fundamentals by building it from scratch in R, then scale up with regtools for production-ready modeling with automatic validation and hyperparameter tuning.

September 16, 2025

Time Series Forecasting Part 4: Practical Forecasting Applications with Confidence Intervals

Demonstrates how to generate forecasts with confidence intervals using ARIMA for stationary data and Holt-Winters for trending data.

September 12, 2025

Time Series Forecasting Part 3: ARIMA vs SARIMA vs Holt-Winters on Non-Stationary Data

Evaluating ARIMA, SARIMA and Holt-Winter models on non-stationary data.

September 8, 2025

Time Series Forecasting Part 2: ARIMA vs SARIMA vs Holt-Winters on Stationary Data

Evaluating ARIMA, SARIMA and Holt-Winter models on stationary data.

September 6, 2025

Time Series Forecasting Part 1: Is Your Data Stationary? A Simple Test That Determines Model Success

The ADF test provides a simple, statistical method to identify whether your data exhibits stationary or non-stationary behavior.

August 31, 2025

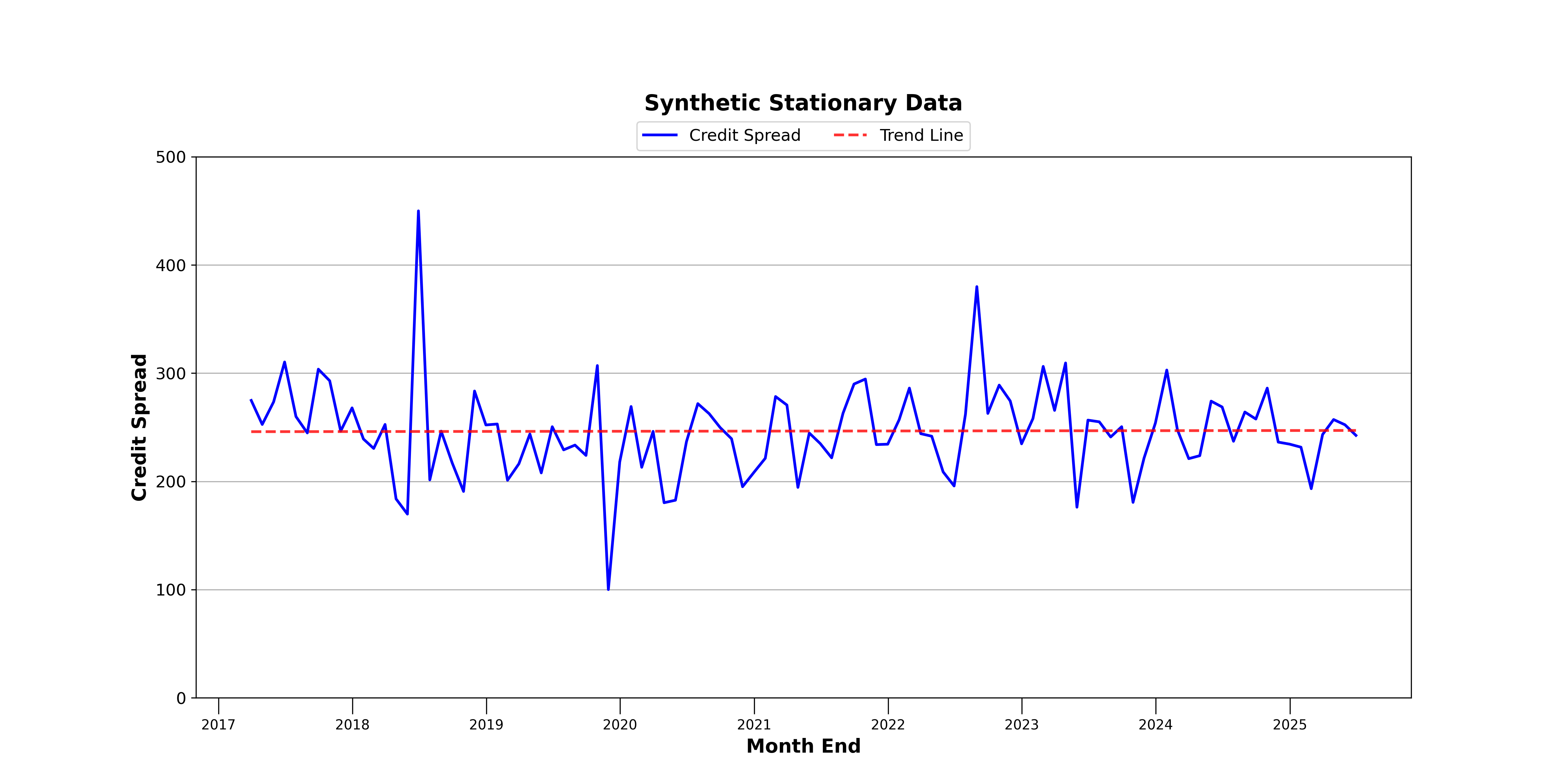

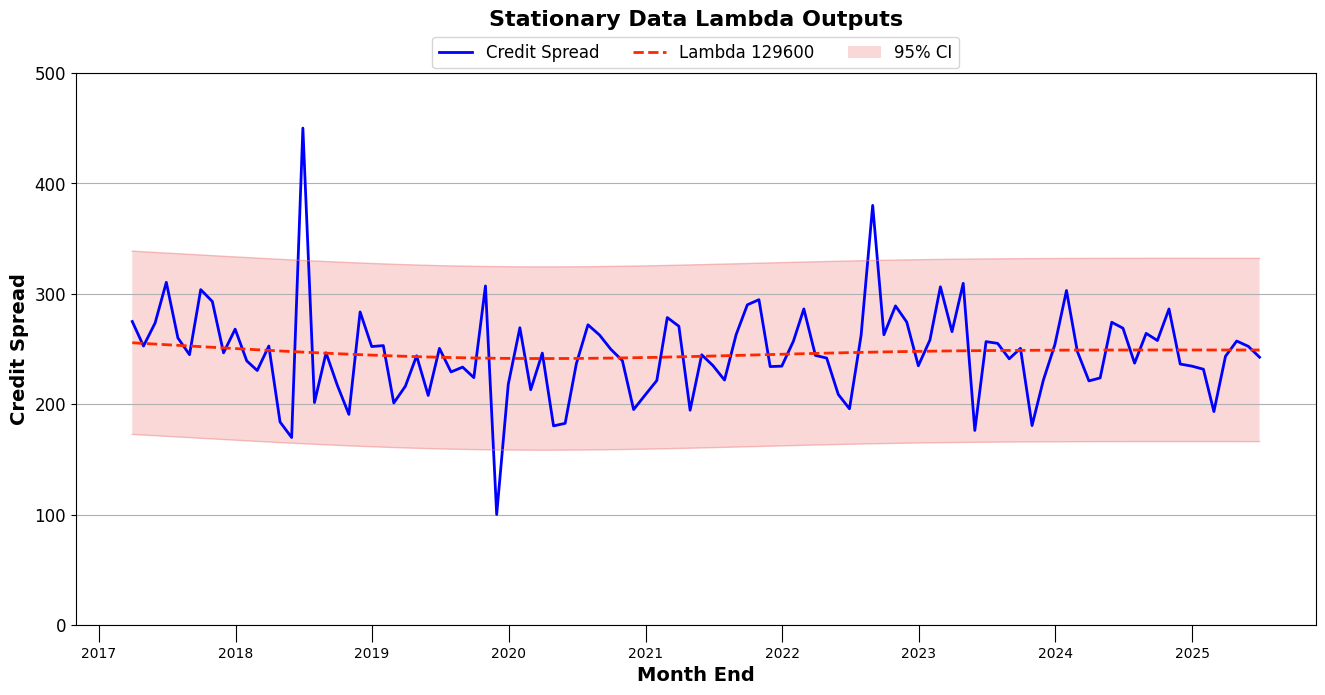

HP Filter Parameter Selection: Evaluating Lambda

An evaluation of the key hyperparameter for HP Filter trend and cycling: Lambda.

August 19, 2025

Put-Call Parity: Synthetic Positions for Building Protected Investment Strategies

This analysis demonstrates how put-call parity creates equivalent portfolio protection strategies through different instrument combinations.

August 13, 2025

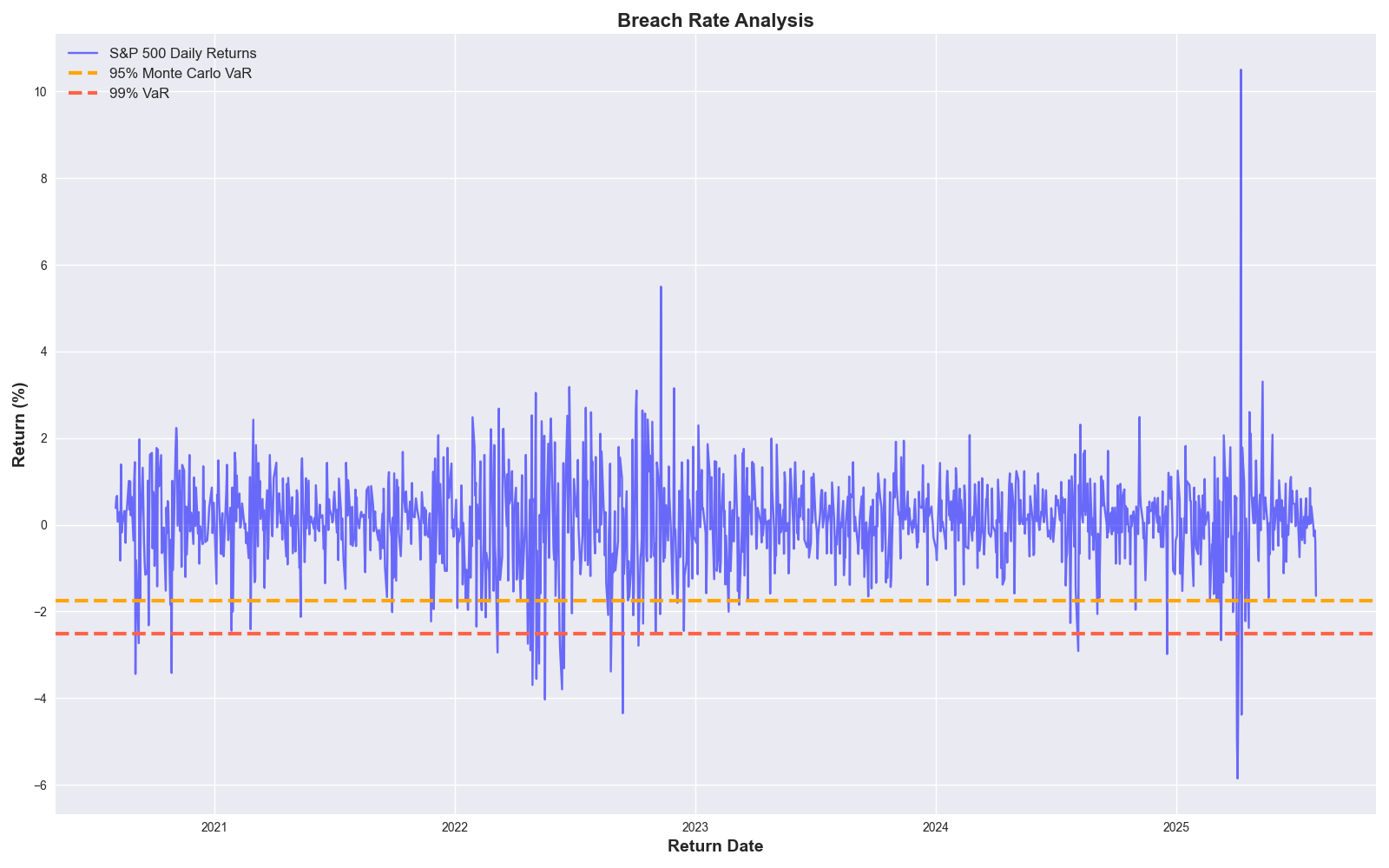

Monte Carlo Simulation with VaR

A practical demonstration of Monte Carlo simulation for calculating Value-at-Risk (VaR) using S&P 500 data, including model validation and limitations analysis.

.png)

.png)