PURPOSE

To measure the risk profile of the S&P 500 and determine volatility metrics for adequate risk management using advanced GARCH modeling techniques.

OBJECTIVE

Determine the risk profile and forward-looking risk characteristics of the portfolio while assessing current market conditions to understand directional risk trends and regime changes.

PROCESS

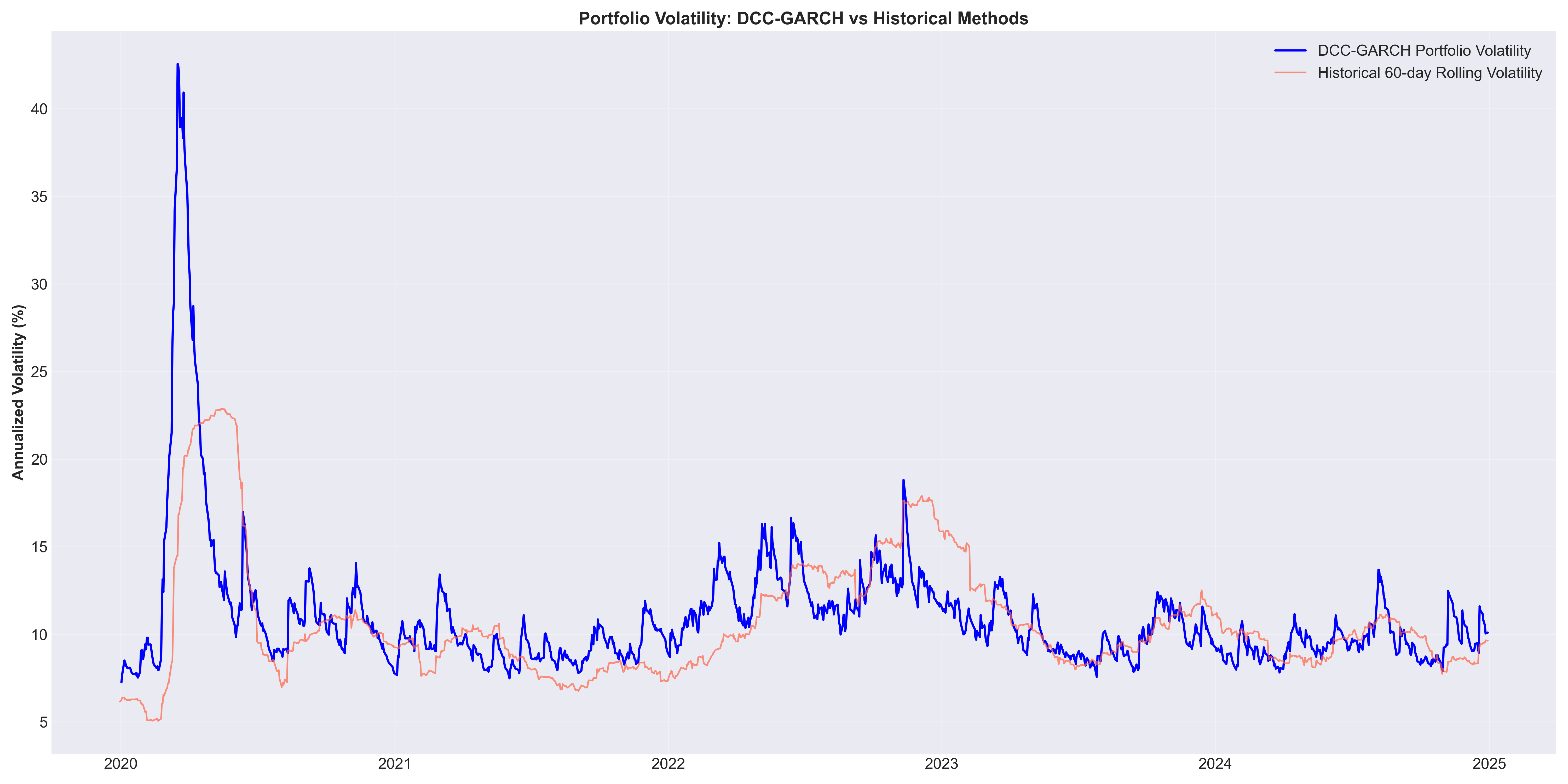

Applied GARCH(1,1) with Student's t-distribution modeling to S&P 500 returns, conducted multivariate correlation analysis with bonds and gold, implemented rolling window forecasting, and performed comprehensive stress testing across multiple market scenarios.

OUTPUT

The GARCH model achieved 100% directional accuracy in volatility forecasting and identified current elevated risk conditions with daily VaR of 2.17% to 3.51% under normal market conditions. Dynamic correlation analysis revealed regime-dependent diversification benefits, with bond-stock correlations becoming more negative during crisis periods when portfolio protection is most needed. Stress testing demonstrated potential daily losses could reach 7% to 12% during extreme market events, providing actionable risk metrics for portfolio management and strategic decision-making.

.png)

.png)