PURPOSE

Identify equity pairs with strong mean-reversion characteristics to detect trading opportunities when stock spreads diverge beyond normal ranges, supporting systematic arbitrage strategies through automated signal generation and real-time monitoring.

OBJECTIVE

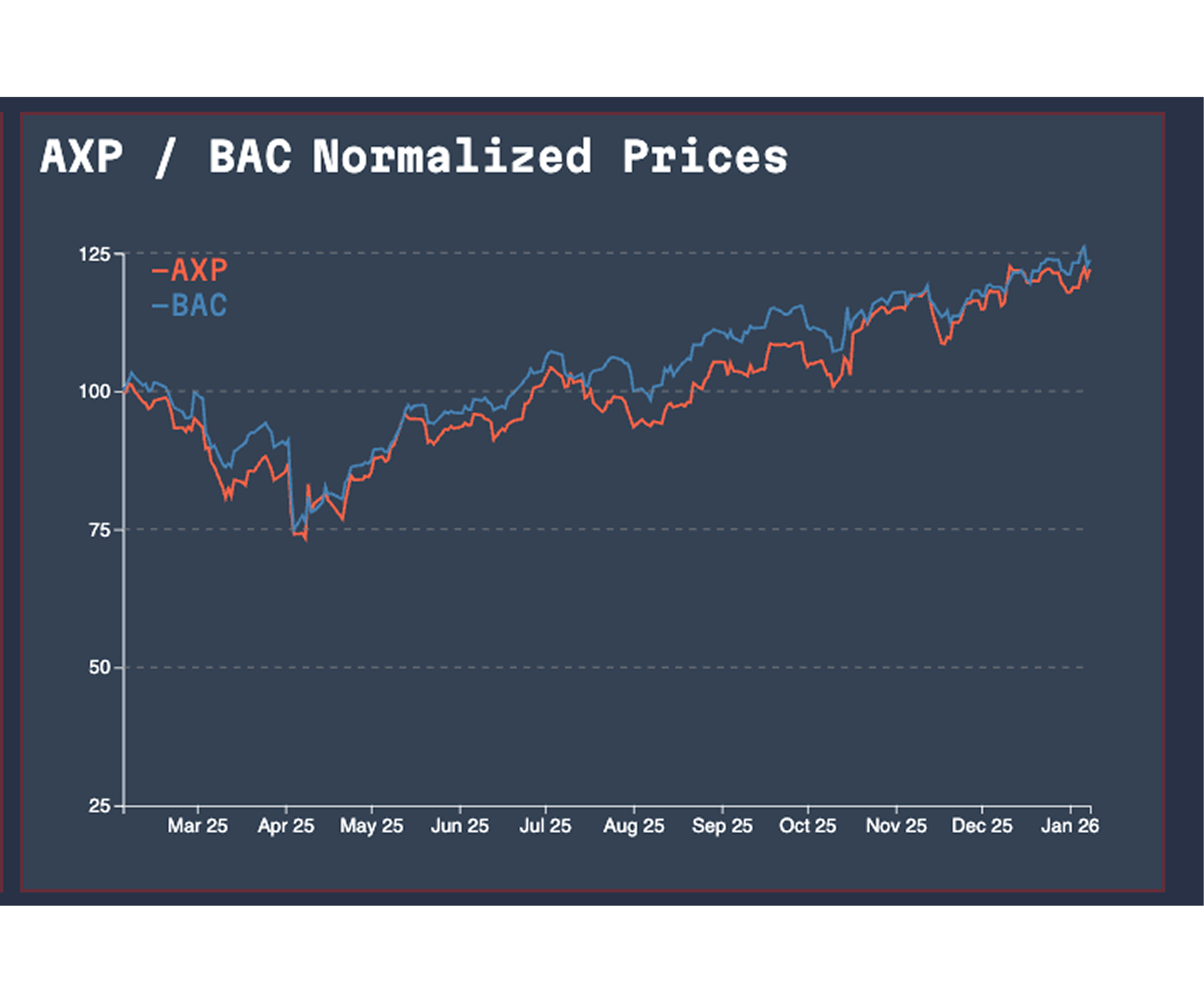

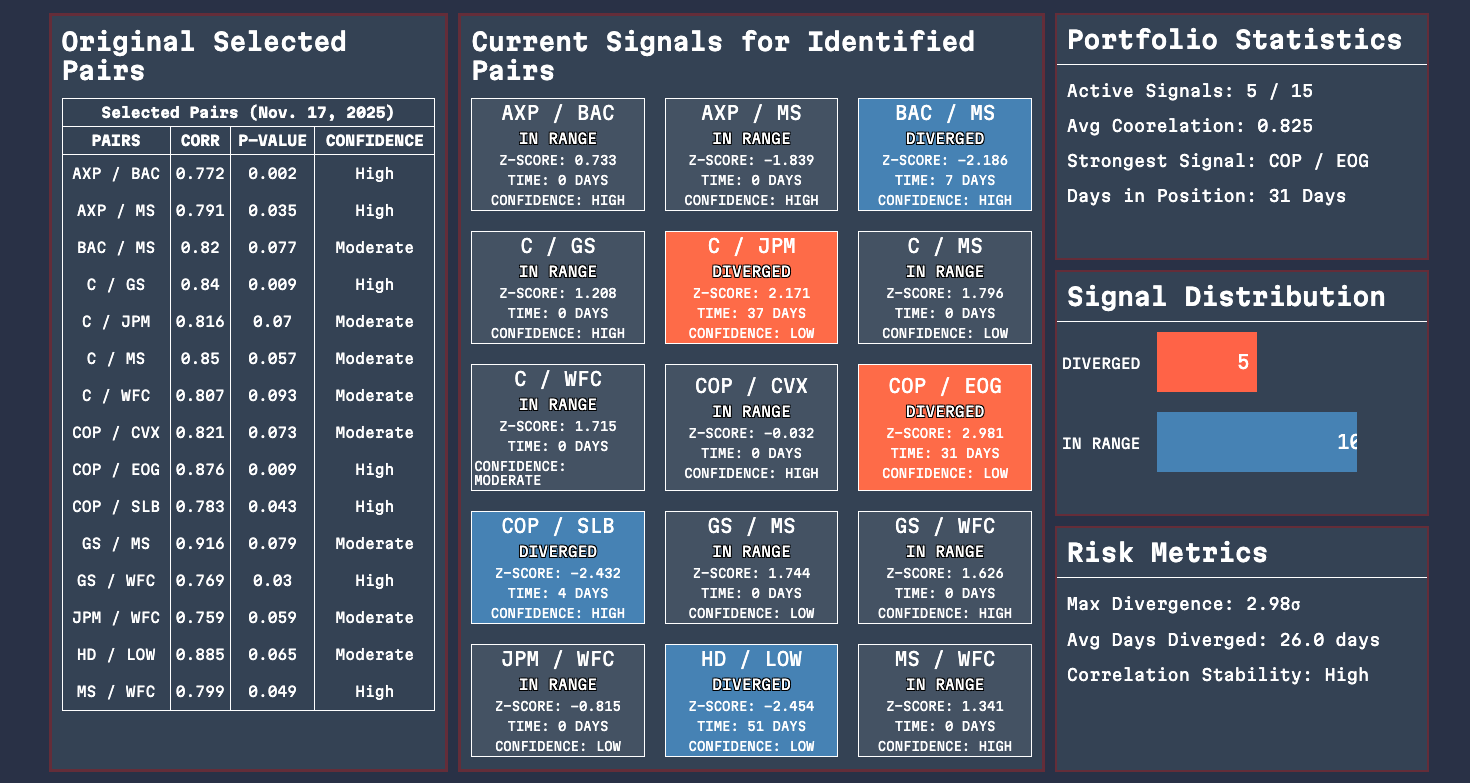

Track 15 equity pairs across financials, energy, and retail sectors using real-time z-score monitoring to detect spread divergences exceeding ±2 standard deviations (σ), generating actionable trading signals with statistical confidence levels and interactive visualizations for trade execution decisions.

PROCESS

Implement serverless AWS Lambda pipeline with daily Yahoo Finance data api ingestion, calculating rolling 252-day correlations and Engle-Granger cointegration tests (p < 0.10) to identify mean-reverting pairs, then deploy interactive D3.js dashboard with real-time S3 data integration for signal monitoring and historical spread analysis.

OUTPUT

Deployed production-grade full-stack platform monitoring 15 pairs with automated signal generation, featuring interactive time-series visualizations, 7-day z-score heatmaps, and mobile-responsive design (768px-1500px breakpoints). Identified high-confidence pairs (p < 0.05, correlation > 0.75) with real-time spread tracking and quantified divergence metrics for systematic trading strategy execution.

.png)

.png)